Everything you need to know to choose a health plan in MA

Topics covered

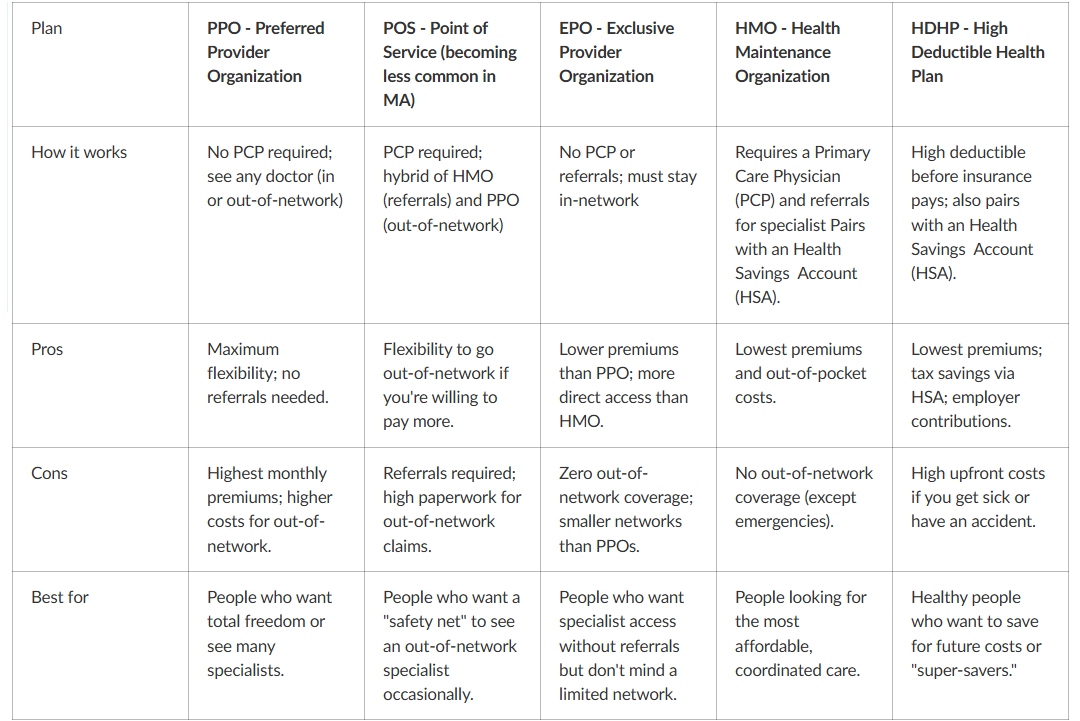

Plan types: HMO vs PPO vs EPO vs POS vs HDHP

Terms that relate to payment: Premium, Deductible, Copay, Coinsurance, & OOPM

Accounts: HSA, FSA, & HRA

Network rules that can cost you money

Common mistakes people make

Figuring out health insurance in Massachusetts can feel like cracking a secret code. When sitting down to choose a plan for the year, you're suddenly hit with a wall of acronyms: HMO, PPO, EPO, HSA.

Health insurance companies use these abbreviations to keep paperwork short, but for most people, it makes it harder to differentiate between plans and understand the implications of their selection. These terms are important- knowing them can mean the difference between a covered visit and being unexpectedly assigned to another doctor.

In this blog, we’ll clear up the health insurance jargon and explain the abbreviations you’ll encounter.

1. Health insurance plan types explained: HMO vs PPO vs EPO vs POS vs HDHP

These are the types of insurance plans you’ll see when shopping for coverage. They determine where you can go for care and the level of flexibility that you have.

If you’re already working with a preferred provider but looking to switch plans, do not succumb to the ease of asking ChatGPT if your provider accepts the new plan that you’re considering. AI is not error-proof, and I’ve lived through the mistake of switching to a plan that was ChatGPT-affirmed but in reality untrue.

The surest way to ensure that your preferred provider accepts a particular insurance plan is to visit the provider’s website, search for “health insurance,” and check the list of accepted plans. Be very discerning - two plans from the same insurer can work very differently depending on the network, the hospital system, and even the specific plan version. Pick up the phone and call your health care provider if unsure.

2. Health insurance costs explained: premium, deductible, copay, coinsurance & out-of-pocket maximum

These are the basic payment terms that one should know when considering an insurance plan.

Premium: The monthly amount you pay just to have insurance. It’s like a subscription; you pay for it even if you don’t use any medical services that month.

Copay: A fixed, flat fee you pay at the time of service, like $30 for a doctor’s visit.

Deductible: What you pay out-of-pocket for most services before insurance starts covering care.

Coinsurance: Your share of the bill after the deductible is met, calculated as a percentage (e.g., you pay 20%, insurance pays 80%).

Out-of-Pocket Maximum (OOPM): This is the most you’ll have to pay in a year. After you reach this amount, insurance pays 100% of your remaining in-network costs.

One important thing to remember: Low premiums might look good, but they often mean higher deductibles or stricter rules. That’s why it’s just as important to understand these terms as it is to pick the right plan.

For a more detailed read on this topic, check out “An Idiot’s Guide to Health Insurance in MA”.

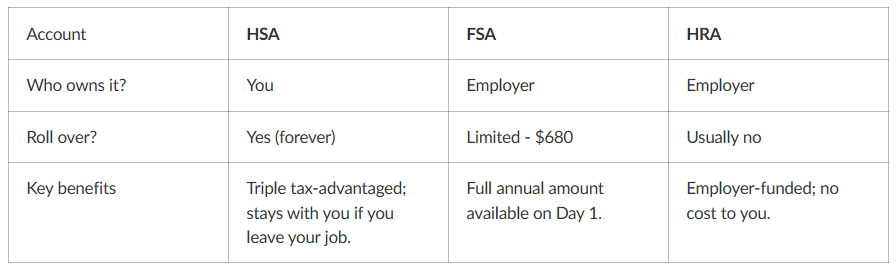

3. HSA vs FSA vs HRA: What these health accounts mean and how they save you money

These are not insurance plans. They are tax-advantaged accounts that help you pay for medical care. Each functions differently regarding ownership, limits, and how the money moves.

Health Savings Account (HSA)

This is akin to a "Personal Savings" account. Many people call the HSA the "Gold Standard" of health accounts because of its Triple Tax Advantage: 1) money goes in tax-free, 2) grows tax-free if you invest it, and 3) comes out tax-free for medical bills.

Unlike other plans, you own the account, so the balance rolls over every year and stays with you even if you change jobs or retire. To unlock these benefits, you must be enrolled in an HSA-qualified insurance plan. Once enrolled, you can sign up for an HSA account. I use Lively.

HSA accounts could be funded up to $4,400 for individual coverage or $8,750 for families in 2026. These limits increase every year, providing one of the few ways to turn a required expense into a tax-free safety net for your future.

Tip: An HSA can be a great way to save for future medical expenses, especially if you’re healthy and don’t expect big bills this year.

Flexible Spending Account (FSA)

This is a "use it or lose it" account. You add money from your paycheck tax-free, but you usually have to spend it by the end of the year. As of 2026, the IRS lets employees contribute up to $3,400 and carry over $680 into the next year if their employer allows it.

Unlike an HSA, which works like a debit card (you can only spend what you've deposited), an FSA is pre-funded. This means your full annual election is available to you on the very first day of the plan year, even before your first paycheck deduction. If you spend the full balance and then leave the company, you are not required to pay the money back - the employer absorbs that cost

Health Reimbursement Arrangement (HRA)

This is a "Reimbursement" fund. Your employer deposits money into an account, and you submit receipts to be reimbursed for medical costs. If you leave the job, the money stays with the employer. Depending on the specific type of HRA offered, the 2026 limits are:

Standard (Integrated) or Individual Coverage HRA (ICHRA): This is the "Classic " HRA paired with a group health insurance plan. No IRS-mandated limit; the maximum amount is determined solely by your employer.

Qualified Small Employer HRA (QSEHRA): This is for businesses with fewer than 50 employees that do not offer a traditional group plan. Its annual limit for individuals is $6,450 per year, and family coverage is $13,100.

Excepted Benefit HRA (EBHRA): This is used to reimburse "excepted" benefits like vision, dental, or COBRA premiums, even if you opt out of the primary group plan. Has a limit of $2,200 per year.

4. In-network vs out-of-network: how insurance networks affect your medical bills

Where you get care can make a big difference. Here’s what you should know:

Primary Care Phycisian (PCP): Your main doctor who coordinates all your care. They are required for HMO and POS plans.

In-network vs Out-of-network: In-network providers have a contract with your insurer to charge lower rates. If you go out-of-network, you might have to pay the whole bill yourself.

Referral: This is like a permission slip from your PCP to see a specialist. It’s common in HMO and POS plans.

Prior Authorization (PA): Approval from your insurance company is required before certain procedures. This is usually required for expensive things like MRIs, surgeries, or specialty drugs.

As of 2026, new federal rules require insurance companies to decide on your Prior Authorization requests faster - usually within 7 days for standard requests or 72 hours for urgent ones - and to give a clear reason if they deny it. These approvals must be sent electronically to your doctor’s system.

5. Common Health Insurance Mistakes That Can Cost You Hundreds (or More)

1. The "monthly price" trap

Choosing a plan just for the lower premium is the most common mistake in MA. A plan that saves you $200 a month in premiums but has a $5,000 higher deductible only saves you money if you never go to the doctor.

You should estimate your total annual cost (12 months of premiums), plus your expected out-of-pocket costs, before deciding.

2. Assuming the insurance site is 100% accurate

Networks change all the time. As I learned with my Tufts and Harvard Pilgrim switch, an insurer’s Find-a-Doctor tool can be out of date. In 2026, some major MA hospital systems have changed which Direct or Select plans they accept.

Always check the hospital or provider’s website directly. Look for a page titled "Insurance Accepted" or "Network Participation."

3. The "Silent" Prior Authorization (PA) failure

Many people think that getting the PA is the doctor’s responsibility. While doctors usually send in the paperwork, you’re the one who gets the bill if it’s denied.

If you’re getting an MRI, surgery, or an expensive brand-name drug, ask your doctor if the Prior Authorization has been approved and if you may have the authorization number.

4. Misunderstanding the "Direct" vs. "Premier" labels

In MA, insurers often use words like Direct, Select, or Value to show a Limited Network. These plans cost less because they exclude some hospitals. Premier or Total usually means you get the full network.

Don’t just look at the brand, like Tufts or BCBS. Check the network tier. If it says Direct, assume a major hospital might not be included.

5. Leaving FSA money on the table

The IRS allows a $680 carryover for 2026, but only if your employer chooses it. If not, any money left in your FSA on December 31st or after your plan’s grace period goes back to your employer.

Set a Health Audit reminder for October. If you have a balance, use it to buy eligible items.

6. Forgetting that the "referral" is a legal requirement

If you have an HMO, which is very common in MA, seeing a specialist without a referral from your PCP isn’t just a mistake- it's grounds for the insurance company to deny your bill in its entirety.

Even if the specialist says they take your insurance, you'd still need that digital permission slip from your PCP in the system.